Does Bonds Upon Maturity Continue to Draw Interest

When you invest in a savings bond, you're making a loan to the federal government. The savings bond maturity is the time at which the government owes you the full amount of principal and interest related to your loan.

Savings bonds are important to understand as basic savings vehicles. Here we'll outline what savings bond maturity means and what to do once your savings bond finally comes due.

Image source: Getty Images.

When do savings bonds mature?

Savings bonds mature at a variety of different times, depending on the series you hold.

Series I savings bonds, commonly referred to as "I bonds," fully mature after 30 years. However, you can redeem them as early as one year after purchase. If you do redeem them early, you'll give up the last three months of interest, so you'll need to make sure you really need the money if you want to cash out early.

Series I bonds offer a fixed rate of interest plusan inflation adjustment. As of November 2021, the I bond rate is 7.12%.

Series EE savings bonds also mature after 30 years. Like I bonds, they will earn interest until they are redeemed. Series EE bonds differ from I bonds in two main ways:

- They offer a fixed interest rate for the life of the bond. The current rate is 0.10% annually.

- They offer a one-time adjustment to double the face value after 20 years of ownership.

Series HH bonds are formerly issued savings bonds that matured after 20 years. The last batch will finally mature in August 2024 since the final HH bonds were issued in August 2004.

Given the nature of savings bond math (more on this later), it's better to hold your savings bonds as long as you reasonably can to take advantage of accrued and compound interest. Allowing your bond to build value over time is a smart move, which is also why you should only dedicate money to savings bonds that you can afford to be without for some time.

Accrued and compound interest

The term "accrued", in the world of savings bonds, is simply another way to say "accumulated." Your bonds accrue interest from the moment you purchase the bonds. On the last day of each month, your bond's value will increase by the amount of interest you're owed for the time you've held the bond.

For newly issued savings bonds, interest compounds semiannually. This means that every six months, the interest you've accrued is added to the bond's value at the beginning of the period. This amount becomes the new (higher) principal, which, in turn, will earn a greater amount of interest over the next period. This is the very essence of compounding, a concept that serves as the bedrock of long-term investing success.

It's critical to note that the longer you hold your savings bonds, the longer you'll accrue interest that compounds over time.

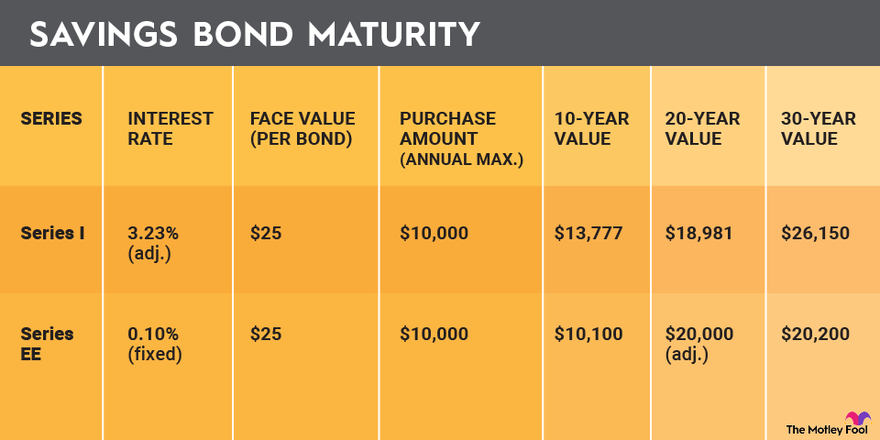

Savings bond value example

In the example below, you can see how a bond builds its value over time. The main takeaway, as mentioned earlier, is that you'll earn more interest and receive maximum value for your bond if you hold it until maturity.

Image source: The Motley Fool

For Series I bonds, the key thing to remember is that the given interest rate at purchase is the sum of a fixed interest rate plus a semi-annual inflation rate. For I bonds issued in November 2021, the entire beginning interest rate reflects inflation alone; fixed rates for I bonds without accounting for inflation are essentially zero.

It's important to remember there is a good possibility that interest rates for I bonds will fall in the future, so the currently offered 7.12% is not guaranteed to stick around for longer than six months. As a result, the table reflects the U.S. long-term average inflation rate, which is 3.23%. As a conservative measure, the calculation also assumes that the fixed-rate portion of I bond interest will remain at zero.

For Series EE bonds, you're guaranteed a fixed rate of interest throughout the life of the bond. The catch here, though, is that interest rates currently offered on EE bonds are extremely low; the government offers a one-time adjustment after 20 years to double the bond's face value.

If you're going to buy EE bonds, it's not really a great idea to buy them for the 10-year interest, but it could be worth your while to stash away lower-risk assets in EE bonds if you have a 20-year horizon for the money.

Remember that savings bonds aren't like crypto or tech stocks. There's minimal risk of catastrophic loss, but you also won't earn huge long-term returns. However, it's good to know that savings bonds are meant to be long-term purchases with benefits for those willing to hold them until maturity. For the right type of saver and for someone who wants to diversify their net worth, savings bonds could make sense.

What to do when your savings bond matures

You've waited for three decades and your bond has finally matured. If you want to cash in your bonds, there are different steps to take depending on the form you hold (paper or electronic).

- Electronic savings bonds can be cashed on the TreasuryDirect website, and you'll receive the proceeds within two days.

- Paper savings bonds can be cashed at most major financial institutions such as your local bank.

If you can't find your fully matured paper savings bond, you'll need to have it replaced electronically by visiting the TreasuryDirect website and filling out the required forms.

You'll need to know the bond's serial number, which acts as a unique identifier. If this is not available, you'll need additional identifying information such as the specific month and year of purchase, the owner's Social Security number, and names and addresses associated with the bond. It may take a few tries, but it's possible to locate the bond even if you've misplaced it.

You can hold your bond once it reaches maturity, but you won't earn any additional interest. On one hand, you can't spend a savings bond without redeeming it, so the value of your bonds would be considered "safe" from that standpoint. On the other hand, you'll miss out on earning interest from other sources if your bond goes unredeemed. With inflation rates as they are now, it doesn't make much sense to hold a bond earning nothing and explicitly losing to inflation with each passing day.

As a final consideration, you'll owe taxes on your bonds when they mature whether or not you redeem your bonds. Make sure to include any earned and previously unreported interest on your tax return in the year of maturity. If you don't, you might face a penalty for underpayment of taxes.

Related investing topics

For best results, hold until maturity

Savings bonds, specifically I bonds, have recently attracted attention due to their higher-than-usual interest rates. For those looking to combat inflation with a very low-risk instrument, I bonds might have a place in your portfolio. Series EE bonds offer very little in the way of inflation protection, but they do provide a one-time inflation adjustment at 20 years.

Generally speaking, savings bonds are most effective when you hold them to maturity because of accrued and compound interest. If you decide to purchase savings bonds, hold them until maturity for best results.

The Motley Fool has a disclosure policy.

Source: https://www.fool.com/investing/how-to-invest/bonds/savings-bond-maturity/

0 Response to "Does Bonds Upon Maturity Continue to Draw Interest"

Post a Comment